As the insurance industry does its best to transform to meet the needs of a new generation of customers, much of their efforts are focused on how to improve upon the existing experience for customers. They are designing new websites, developing apps, and exploring technology like AI, chatbots, and machine learning, trying to make the process of buying insurance less cumbersome and up-to-date with consumer expectations. While these efforts are well spent, and certainly necessary, they don’t go far enough.

On January 31, we teamed up with Coverager to discuss how integrating the concept of “community” into how insurance is bought, sold and operates not only delivers more value for customers, but also helps the next generation of customers think about insurance in a new way.

You can watch the full webinar and download the presentation slides here.

Insurance & Community

Creating authentic connection in the age of hyper connectivity

Resonating with values to deliver more value

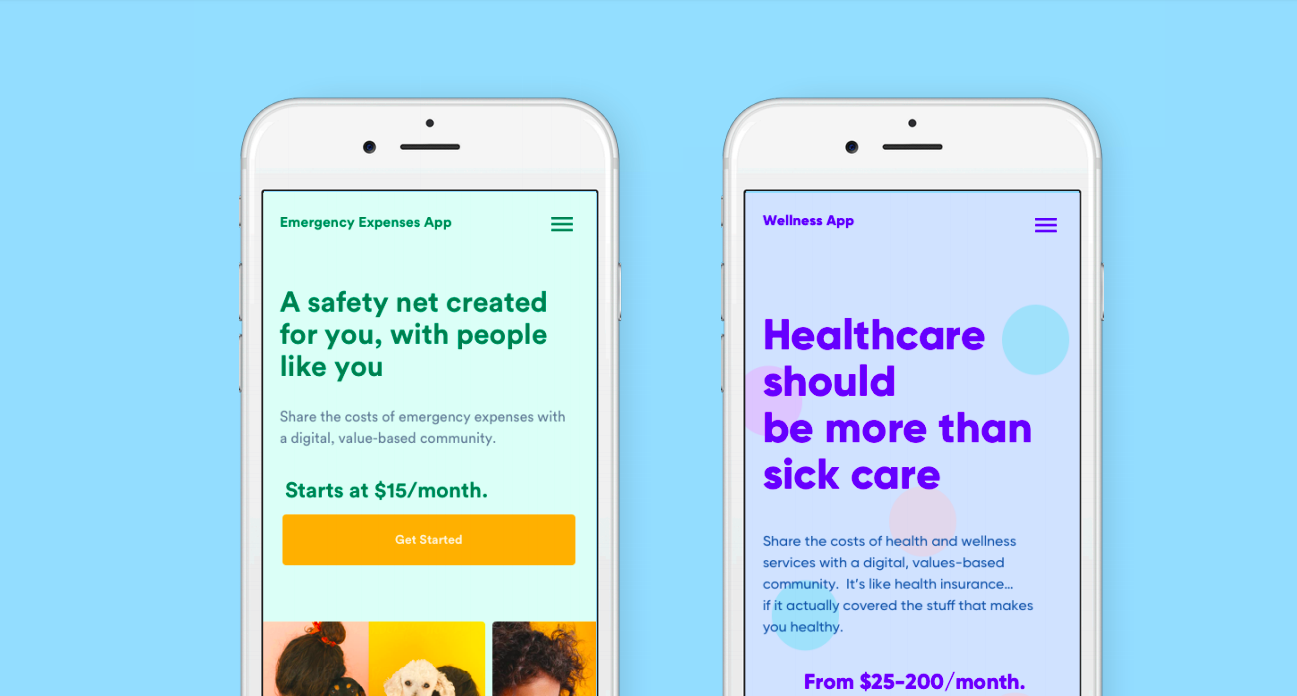

Cake & Arrow kicked off the webinar, sharing insights from both qualitative and quantitative Millennial research we have conducted over the past nine months, as well as prototype demos of two insurance product concepts we recently designed and tested with Millennials.

In our first round of research we were able to hone in on some of the main challenges facing Millennials today–two of the most prominent being financial stability and security and uncertainty in the future. These were areas we believed the insurance industry was already well-positioned to offer value. In theory, good insurance products not only provide more financial stability and security, but they also curb uncertainty in the future. The fact that these needs were not currently being met for the Millennials we surveyed, however, meant that insurance wasn’t doing it’s job, or, at the very least, not doing it well enough.

Making Insurance Work for Millennials

Millennials are about to rule the world. Is the insurance industry ready?

Helping people think about insurance in a new way

By and large, both products tested incredibly well with both groups of participants, and we were able to validate our hypothesis around how resonating with values delivers more value to users, and learn other interesting insights around community that will guide product development in the future, findings which were shared by Lisa McGee, our lead experience designer who oversaw the research during the webinar. Ultimately we found that by surfacing the community aspect of insurance, we were able to help our research participants think about insurance in a new, and largely more positive way.

To see more of the prototypes and access the full insights from our user testing, you can download our slides here.

From research to reality

While our presentation featured research and insights from the testing of hypothetical community-based insurance products, the latter half of the webinar focused on two new startups that are already in market exploring how insurance and community intersect in real life.

Eusoh – Insurance is basically crowdfunding

Allen Kamrava is the CEO and founder of Eusoh, an alternative to pet insurance that allows customers to organize themselves into communities to share the costs of pet-related medical expenses.

In the webinar, Allen shared how his experience as a doctor working with patients, many whom had given up on health insurance altogether, inspired his idea for Eusoh.

“Health insurance is universally accepted as a broken model,” he explained. He sees one of the main problems with insurance being the giant fund created by premiums, which both insurance companies and providers are incentivized exploit. He explained how when healthcare providers see this giant fund of money, they will run every test in the gamet, even providing unnecessary services so they can charge for them, thus driving up the cost of healthcare. “The huge fund pollutes the process,” he said.

With Eusoh, Allen took what he thought was wrong with health insurance, and attempted a solution, but applied it to pets. He likes to refer to it as crowdfunding. Rather than collecting premiums every month, Eusoh collects a monthly subscription fee (this is how the company makes money). Users group themselves into communities who then share costs of their pets’ medical expenses, for a fraction of the price of regular pet insurance (in December, when a large amount of pets ended up in the hospital, the shared cost split among members was only $2.88). There is no “fund” to take advantage of, because community members pay only for the medical expenses accrued at the end of the month, rather than putting money into a pool “just in case” something happens. In this way, Allen believes that Eusoh can not only keep costs down, but provide members with the social value of knowing they are helping other pets.

Because Eusoh is not technically insurance, they are able to bypass regulation, and there is no underwriting or preexisting conditions or any of the other usual insurance hangups. As far as who gets to join a group, Eusoh leaves it completely up to the groups themselves to decide whose pets are covered. “We are completely agnostic as a system,” Allen explained.

For Allen, the community aspect is a big part of what keeps people honest. “We wanted people to be accountable. And while we know that in regular insurance, most people are good actors, we wanted to drive home that you aren’t taking from some giant fund, you are spending you are taking from other people’s wallets.”

Wilov – A digital experience doesn’t mean a dehumanized experience

Wilov, a pay-as-you go car insurance company based in Paris, was born out of CEO and founder Pierre Stanislas’s own personal dissatisfaction with insurance. Almost a millennial himself (he was born in 1980), he wanted to develop an insurance product that would meet his own standard of what a product or service should be–simple and transparent, offering value at a fair price, accessible at his fingertips via an app and most importantly, an experience.

During the last half of the webinar, Pierre shared how from his perspective, a big part of what makes Wilov an experience is community. Wilov isn’t just regular car insurance. It’s car insurance for people who share the same approach to mobility. “What we really wanted to build was a community, a community which shared a common sense of using their car responsibly–because it’s good for the environment, because it’s fiscally responsible–and then bring them a common product.”

While it’s important that everything happens digitally via the app, Wilov reinforces a sense of community by ensuring there is a thoughtful human touch to all of the company’s interactions with their customers. “A digital experience doesn’t mean a dehumanized experience,” said Pierre. Onboarding, for example, happens with a community manager over video chat, and these same community managers continue to interact with customers throughout the duration of their policies, responding to everything from social media comments to questions about their policies.

Even with the flexibility and the community aspects offered by their insurance, Pierre was quick to point out that at the end of the day, car insurance remains a very competitive market, with aggressive pricing. “We offer a quality, luxury product at a fair price, if you don’t use your car everyday,” explained Pierre. “They come for the price, but they stay for the community and for the experience–and then they talk about it.”

The proof is in the pudding. The social pudding. Over 50% of Wilov’s growth is organic, coming from referrals and word of mouth, and with a star rating of 4.8, the Wilov app is the top rated insurance app in France and has double the number of user comments as AXA, a company with millions of customers (compared with Wilov’s thousands). Not to mention they also recently became the first insurance app to be awarded Apple’s “editor’s choice.” As Coverager’s Shefi Ben-Hutta, host of the webinar noted, it seems like they are doing everything right.

__

Even as the insurance market becomes increasingly crowded with new insurtech startups, there remains enormous opportunity for carriers and insurtechs willing to go the extra mile–beyond fancy digital interfaces and sleek new technology–to connect with customers on a deeper level, not only making their lives easier, but making them better, more fulfilling, and more meaningful. Making community an integral part of insurance will deliver value to customers at the highest level, help people think about insurance in a new way, and push insurance beyond the level of product, to make it an experience for customers.

A full recording of the webinar, along with access to the complete slide deck is available for download via this link.